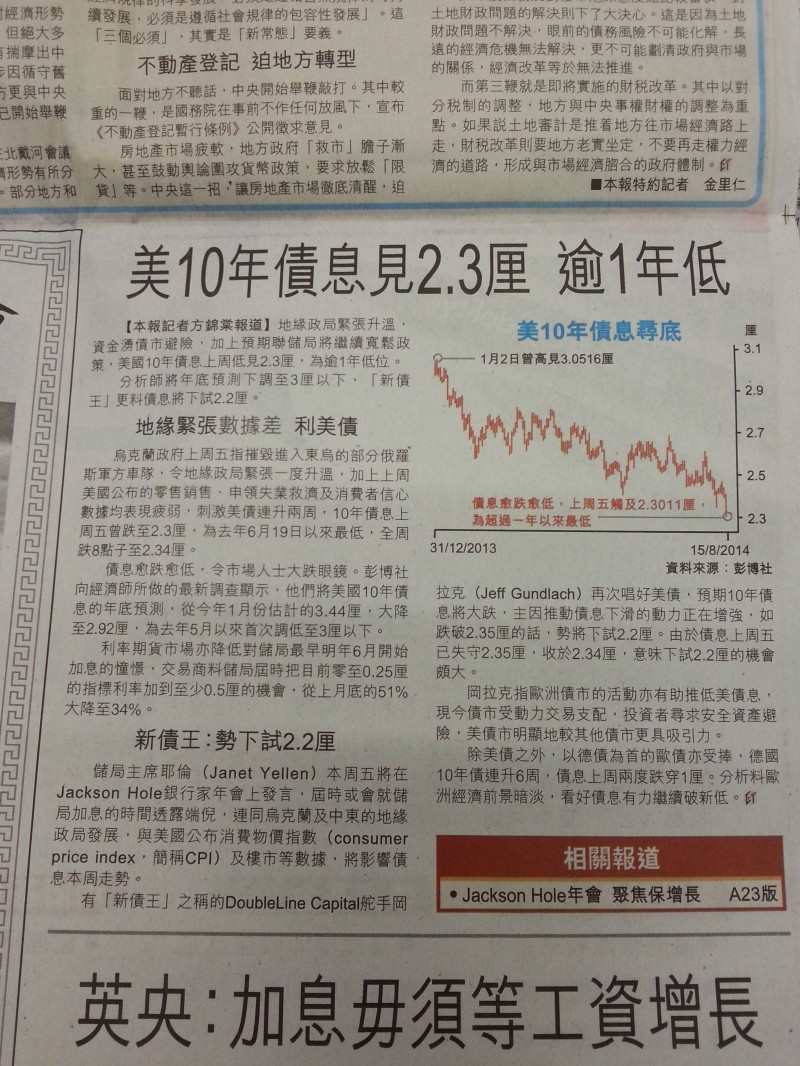

Oscar 兄,

指教唔敢當, 不過大家可以討論吓:

1. "10年債息在2-3厘上、下浮動,是否意味著美國將長期保持低息?"

長債與聯邦基金利率沒有直接關係, 所以不會對FED fund rate 有任何啟示。 個人認為現在維持在2~3厘, 只是對之前從1.3% 升至 3% 的中期調整, 長達30債息下跌大周期, 在前年應已經完結。

2. "10年債息和(美國)按揭利息有何關係?”

請注意是美國而不是香港按揭利息。 要解釋會好長, 所以我懶惰在網上抄了一段, 希望是唔好介意。

The traditional, residential 30-year mortgage is VERY similar to a bond investment. There is a long-term investment horizon, with fixed cash payments over the term of the note. But the principal is returned incrementally during the life of the loan.

So, since mortgages are ‘more risky’ than the 10-year treasury bond, they will carry a certain premium that is tied to how much more risky an individual is as a borrower than the US government.

And here it is… no one actually directly changes the interest rate on 10-year treasuries. Not even the Fed. The Fed sets a price constraint that it will sell bonds at during its periodic auctions. Buyers bid for those, and the resulting prices imply the yield rate. If the yield rate for current 10-year bonds increases, then banks take it as a sign that everyone in the investment community sees some sign of increased risk in the future. This might be from inflation. This might be from uncertain economic performance. But whatever it is, they operate with some rule of thumb that their 30-year mortgage rate for excellent credit borrowers will be the 10-year plus 1.5% or something. And they publish their rates.

,當

,當 。

。